Last week I gave a presentation to the leaders of some women’s health advocacy organizations about where the U.S. healthcare system is heading, i.e., where we go from the current situation with the A.C.A. We had a great discussion, and the organizer of the event emailed me afterward to say, “Amazing is all I can say. You are the first person who could speak to [the] ACA in which people listened and engaged.”

Some of the key points I made included:

- Focus on the future. Don’t relive the past.

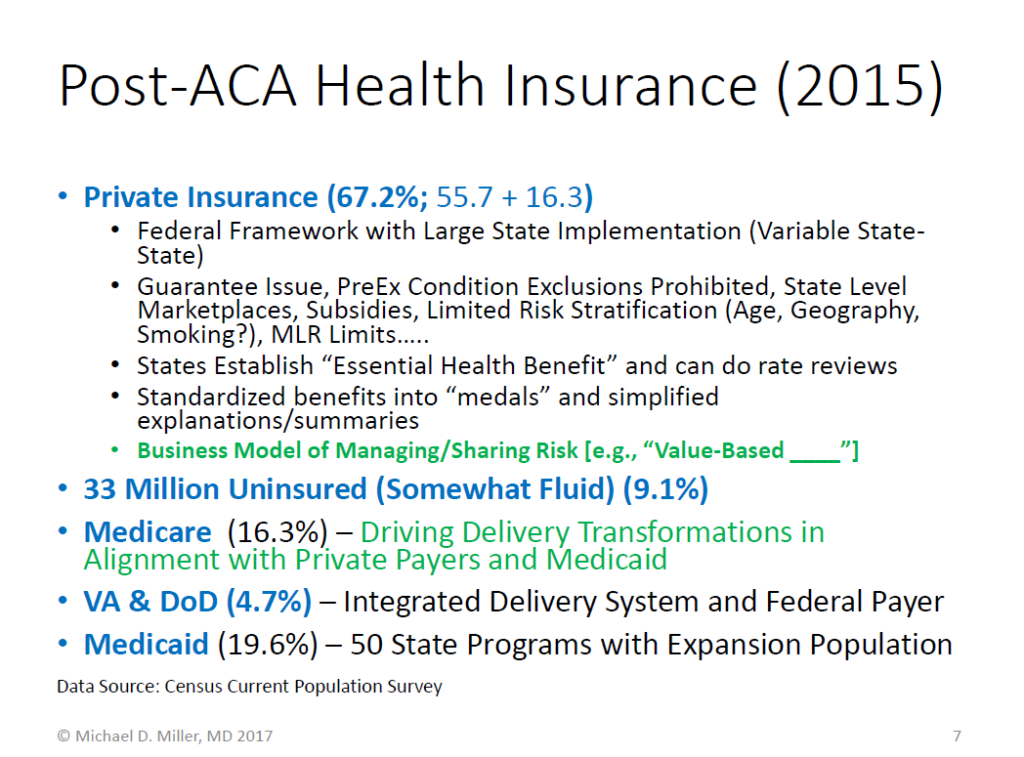

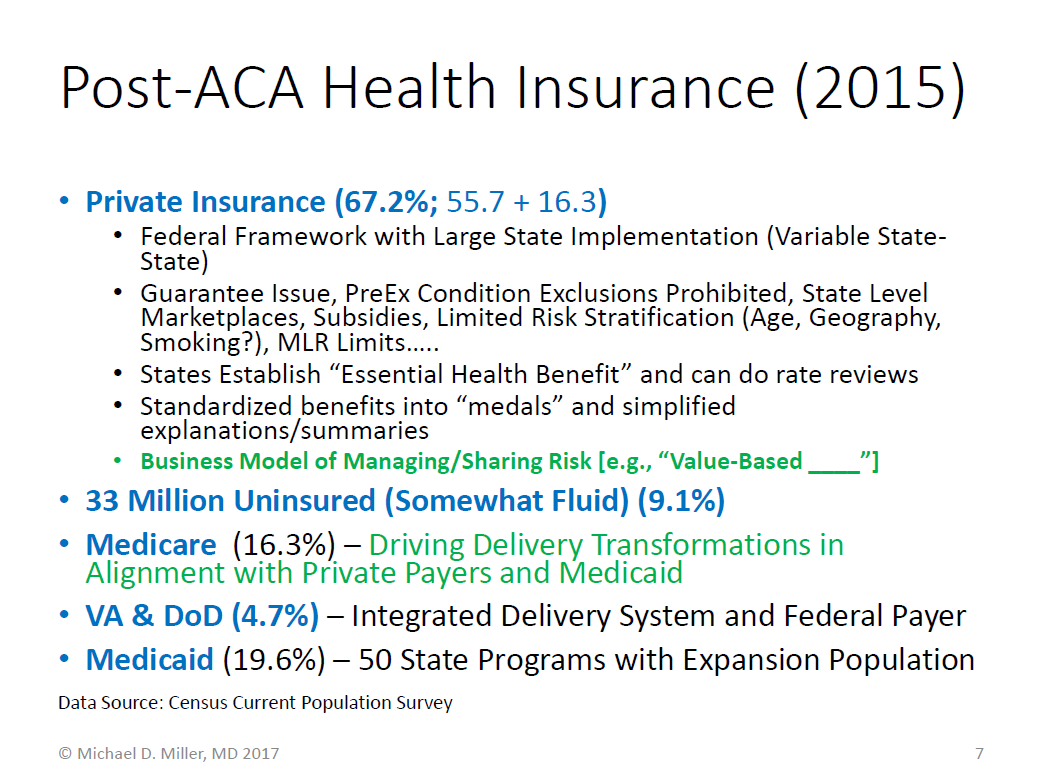

- Move forward from today’s strengths and weaknesses. The slide below describes health insurance coverage for 2015 showing dramatic increases in coverage in individual insurance and Medicaid, and a decrease in the uninsured. [Note: The Census data indicates any insurance status during the year, which is why the total is more than 100%.]

- Are we more of less broken? Some “so-called” pundits have characterized the current situation as “broken.” To move forward, it is important to consider whether or not the current system is more or less “broken” than it was in 2010 when the A.C.A. was enacted, or in 2014 when most of its provisions started.

Several of the less broken aspects of the current situation are:

- The business model for health insurance is now based more on managing risk rather than avoiding risk, which was a major focus before the A.C.A.

- Access to insurance – particularly for individuals – is now much more reliable and dependable. The A.C.A. created a national floor for insurance practices, with state level implementation and augmentation. This was the focus for the “Patient Protection” part of the A.C.A. i.e., the original title of the law was the Patient Protection and Affordable Care Act.

- Descriptions of insurance plans are now more standardized and easier for consumers to understand.

- Medicare’s Hospital Trust Fund is now projected to be solvent for 11 more years than before the A.C.A., and the Medicare Part D benefit was significantly improved, with the coverage gap (a.k.a. “donut hole”) being filled.

Several of the still broken or problem areas in the current situation are:

- Affordability is still a major problem. This is – and was – a problem for many individuals, as well as some companies that discovered in the midst of the Great Recession (2008-2010) that their healthcare costs were eating deeply into their profits. [Note – polling has long indicated affordability as a priority issue, which is why it was called the “Affordable Care Act.” However, affordability takes much longer to achieve than access, which was the case for the A.C.A.’s model in Massachusetts, where affordability is still being addressed.] Within the A.C.A., affordability for lower income people was addressed with subsidies, but overall costs are slowly being addressed with improvements in healthcare delivery – primarily through public-private alignment in new payment models that are driving greater “value” in healthcare. It is also worth noting that this concept of value is at the core of the new Medicare physician payment framework created in the MACRA law, which had large bipartisan support in Congress.

- State-to-state implementation has been very variable, with some states doing a good job in creating more stable insurance markets, and others facing low numbers of insurers in their individual markets.

- Requirements for coverage of certain benefits, and how risks are segmented or shared across populations, are potential areas where changes could be made to address perceived inequities, reduce government spending, and lower costs for some people – but also increase costs for other people. For example, changing the age ratings from 3:1 to 4:1 or 5:1 would expand risk stratification with younger people paying less and older people paying more. Similarly, excluding certain types of benefits from the required “Essential Health Benefits” (which are currently set at the state level within federal guidelines), would decrease costs for people who don’t ever use those benefits (such as contraception or organ transplantation), while increasing costs for people who do use those services. However, such “insurance by body part” practices could also cause insurers (and at risk providers) to build business models around avoiding risk rather than managing it.

Conclusions: The A.C.A. fixed several problems with the U.S. health insurance markets and improved access to health insurance. However, it also accentuated or created some other problems because of its innate structure (e.g., “inartful drafting”), hyper-partisan political advantage seeking, and the normal evolution of insurance business practices. For example, those three factors combined to undermine individual insurance markets in some states because of HHS’ inability to fully make risk corridor payments: The law was not explicit about HHS’ authority, Congress specifically prohibited HHS from shifting funds to make those payments, and many insurers had business plans for the A.C.A. marketplaces with losses in early years to build market share, while expecting to recoup those losses both through the risk corridor payments and higher premiums in later years. The result has been that most of the new non-profit insurance companies created under the A.C.A. (COOPs) failed, and many existing insurers pulled out of markets where they had significant losses, leaving fewer options for consumers. It should also be noted that some insurers have done well in the marketplaces using networks and benefits more similar to Medicaid than large company group health insurance plans, while at least one insurer apparently pulled out of several markets as a positioning strategy to try and bolster their merger plans.

Thus, the A.C.A. transformed what was essentially becoming a two-tiered health insurance market (Medicaid and group health insurance plans) into a three-level system, with a more structured middle tier for individual insurance that looks like a hybrid between Medicaid and large employer health plans. One of the A.C.A.’s successes (although perhaps temporary) was this middle tier, which had been rapidly disappearing in most parts of the country as premiums escalated and people with non-trivial pre-existing conditions were excluded from buying insurance. In 2010, when layoffs were common and the “gig-economy” was expanding, the shrinking supply side of the market for individual insurance not only accentuated the problem of “job lock,” but it also undermined state and federal efforts to control health spending since so many people were “out” of the insurance system.

Are “we” better off than “we” were four years ago? That depends on who “you” are, and what you expect your situation to be in the future.

- For individuals with health insurance through large groups (such as large companies), things are probably about the same as they would have been without the A.C.A. While premiums and deductibles are almost certainly higher, better information about quality of services is available, and there is more access to things like telemedicine – both of which would have occurred to a similar degree without the A.C.A.

- For low income individuals, there are now subsidies to buy insurance, or access to Medicaid (in some states).

- For middle-class people buying insurance on their own, they now have assured access to buying and keeping insurance, although in some cases their costs have increased more than what would have occurred without the A.C.A. in part because they have expanded benefits under the A.C.A.’s requirements. But without the A.C.A., costs for individuals and small groups could have been very dependent upon their age, costly illnesses, or injuries, which could have dramatically increased their premiums, or caused them to lose insurance coverage for specific body-parts or entirely.

- For people with Medicare, things are better since the Part D donut hole is getting filled, and Medicare is driving new quality improvement initiatives, which are also benefiting people who are not on Medicare since many are being done in conjunction with Medicaid programs and private payers.

Bottom Line:

- So, are “we” as a nation better off? Overall, we have a clearer picture of the problems and more tools to try and improve (if not totally solve) the problem areas like affordability and quality.

- Will making productive changes be easy? No.

- Can positive changes be made while extracting great savings from the health insurance and healthcare delivery systems? Not quickly – but possibly over the long term.

- Can changes be made in 2017 so that no other changes will be necessary for many years? No. Like trauma surgery, the patient needs to be stabilized, and then multiple surgeries (targeted towards the problems of greatest urgency and long-term benefit) need to be done over time to improve the functioning and long-term capabilities and viability of the patient. Trying to do everything at once can lead to serious morbidity and mortality, and would be more traumatic and expensive, and waste more resources than a measured and planned approach.