Healthcare issues ranging from national health reform to stem cell research have become a major force in political rhetoric – often overwhelming substantive information. This creates challenges for individuals and organizations seeking to achieve positive changes as their communications are swamped by election-driven messaging.

Creating and implementing successful communications programs in this turbulent environment is easier when the principles of “loss aversion” and the factors affecting the adoption of innovations are used constructively.

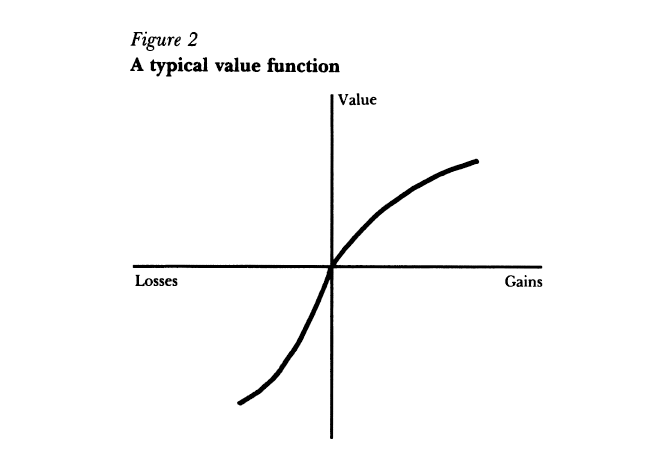

Loss Aversion & Campaign Messages: Swinging Votes Not Actions

Campaign communications – particularly negative messages – are very effective because they use loss aversion principles to leverage people’s reluctance to embrace change.

I have repeatedly heard that people need to believe they will receive a gain that is twice as large as their potential loss before seeking to make a change. However, that 2:1 ratio is derived from some specific social psychology experiments, while loss aversion research demonstrates that the ratio varies depending upon the magnitudes of the risks and rewards for the individual. For example, many people would willingly wager 10 cents on a coin flip if they could win 11 cents by guessing correctly – if nothing else just for the “fun” of playing, and because losing 10 cents isn’t a big deal. However, very few people would wager $1,000,000 on the same coin flip for the chance to win $1,100,000 – even though the odds and the loss-gain ratio are the same, (and in the player’s favor), because the significance of the risk is much greater.

Source: Kahneman et. al. 1991

While these principles are not unique to healthcare, their power for influencing people’s perceptions and actions is greater for healthcare issues because of healthcare’s very personal nature and most people’s impression that they have some healthcare expertise acquired through first-hand experience. [Reader Participation: Insert your story here about a friend or relative who has “educated” or “advised” you with a personal healthcare story, or how someone – perhaps a stranger – has offered healthcare advice based upon something that happened to them, or someone they knew, or they just heard about from someone else.]

The principles of loss aversion make it very, very difficult for potential short-term and individual gains to be the foundation for effective communications campaigns about healthcare improvements for the following reasons:

- Loss aversion means that most people are going to want to see a potential gain that is a multiple of the potential loss – and those most affected by a proposed change will see the potential loss as much more significant, and thus require an even larger potential gain in order for them to not oppose it. (And those most affected will also be the most active and vocal in their opposition.)

- For most people, healthcare changes have significant levels of perceived personal risk – whether it’s changing their health insurance benefits, choice of physicians or hospitals, how they can obtain access to new or experimental treatments, or even very specific changes such as stem cell research, abortions, end-of-life counseling, genetic or autism screening, etc.

- While potential losses are well understood by most people – since they know what they currently have and realize that change will be “something different” – potential gains are usually much harder to visualize and believe in. (This is why the current Administration has said that under the new health reform law people can keep their current health insurance plans if they like them.)

- People’s trust in government and large organizations, (e.g. corporations), has plummeted in recent years, greatly reducing people’s confidence that changes advocated by these sources will actually produce the promised gains. Specifically, in “calculating” potential losses and gains most people will greatly discount potential gains from government or corporate initiatives. For example, suppose a proposed government healthcare change is described as having a gain of 10 and a potential risk of 3. [These numbers are obviously only arbitrary representations of the magnitude of how potential changes might be valued.] This change might be seen as having a gain-risk ratio of 10:3, but a general distrust of government actions could discount the potential gain to 25%, (which is about where Congress’ approval rating is right now), resulting in a perceived gain-risk ratio of only 2.5:3 – and this assumes that people don’t inflate the potential losses because of their low opinion of government, which could make the perceived ratio 2.5:6 or 2.5:9. Clearly this is not a situation where people would eagerly support a change in something as important as their health.

This means that even for a proposed change where the best projections indicate significant benefits to many, many people, any individual or organization who opposes the change, (for political or other reasons), has a very easy time crafting messages and images that are very effective in undermining support for the proposed change. (For example, the combination of the following phrases has been effective in undermining support for the new health reform law: “Government Takeover,” “Death Panels,” “Unconstitutional,” and “You Lie.”)

Overcoming Loss Aversion and Negative/Counter Messaging

The solution to overcoming such undermining messages that play on people’s concerns about losing what they have (and know) – as well as their mistrust of governments and other large organizations – is to present proposed changes in ways that expand people’s confidence in and understanding of the potential gains, while also minimizing the perceived loss potential. One way to do this effectively in a communications strategy is to address the 5 factors influencing the adoption of innovations that Rodgers first described in the 1960s:

- Relative Advantage

- Compatibility

- Simplicity

- Observability

- Trialability

[These are derived from Rogers 2003 book and it’s earlier editions, and described by Dealy and Thomas in their 2006 book.]

Selling Health Reform as Positive Innovation

Shifting to a “selling” campaign that incorporates these factors – while minimizing the potential affects of loss aversion – moves the communications dynamic away from the slippery losing slope of loss aversion’s context to one that is more favorable to thinking about the longer-term and more tangible benefits of the proposed changes. For example, the broad communications campaign for the bipartisanlly supported Medicare prescription drug benefit, (Part D – enacted in late 2003, benefits started in 2006), emphasized how much individuals would save, rather than the long-term value and security of having insurance – which is what Part D plans are, they are insurance, not a discounted purchasing scheme. (A USA Today article stated that an average person who enrolled in a Medicare Part D plan would save $1,100 in 2006.)

The Result: While people who did purchase Part D plans were generally happy with their plans, about 10% of Medicare beneficiaries (~4.5 million people) didn’t have prescription drug coverage in 2007 despite some plans costing less than $10 per month. The large number of people who decided to not purchase this very low cost insurance is even more striking because individuals’ premiums increase by a “penalty” of 1% per month for every month between their initial period of eligibility and their enrollment date. (This penalty is to reduce adverse selection, which occurs when people wait until they are ill before getting insurance.) Unfortunately, the number of Medicare beneficiaries without drug coverage doesn’t appear to be declining – in 2010 it was still about 10% of beneficiaries, and this compares very poorly to the very low percentage of people who declined Medicare Part B coverage.

The significant number of Medicare beneficiaries who decided not to purchase a Part D plan could be due to their aversion to a perceived loss being stronger than the positive messages used to sell the benefits of the plans. This imbalance results from the gains being presented as short-term financial savings, (rather than the long-term benefits of having insurance), and thus didn’t utilize the factors for improving the adoption of innovations, i.e., Part D insurance plans is comparable to other insurance they have, it is not complicated (except for the initial large number of choices), they can observe it, the plans can be tried, and the insurance provides a significant relative long-term advantage.

Bottom Line – Sell the Value & Spirit, Not the Calculation

The bottom line is that selling the value of healthcare changes – whether it’s national reform or narrow innovations – needs to encompass broader, longer-term, and tangible values, rather than short-term calculations that may be both uncertain and not believed, while also deflecting and undermining opposing arguments, i.e. capitalize on the factors that ease the adoption of innovations while minimizing people’s inherent aversion to potential losses.

And in closing, (at least for this posting), how these principles were used in a negative way to sell a non-healthcare change might be a useful illustration:

Buying a house with an unaffordable mortgage was seen as OK before 2008 because the potential for loss was believed to be very small – since prices were rising and foreclosures were rare so there was very little to trigger an aversion. And owning a home is compatible with most people’s desires and daily lives, home ownership is observable, renting is akin to a trial of ownership, brokers and agents made it all very simple, and home ownership has potentially great financial and social advantages. However, in retrospect it’s clear that purchasing a home was vastly wrong for many people – and potentially involved outright fraudulent communications – because they had been led to believe in illusory loss-gain (a.k.a. risk-benefit) calculations.

The large number of people who decided to not purchase this very low cost insurance is even more striking because individuals’ premiums increase by a “penalty” of 1% per month for every month between their initial period of eligibility and their enrollment date.